Empowerment Series: How a HELOC Gives You Financial Flexibility

August 15, 2018

Member Advisors with Unison Credit Union help people in the Fox Valley discover all sorts of personal finance solutions. But, one of the most overlooked, misunderstood, and flexible options is a home equity line of credit, or HELOC.

Pending approval, a HELOC is available to all homeowners1 and allows them to use equity in their home to access funds, but there are some important differences when compared to a home equity loan.

To get a better understanding of how a HELOC works and how you can use this unique financial product, Member Advisor and Branch Manager Erika Arnoldussen explains the details and the potential advantages.

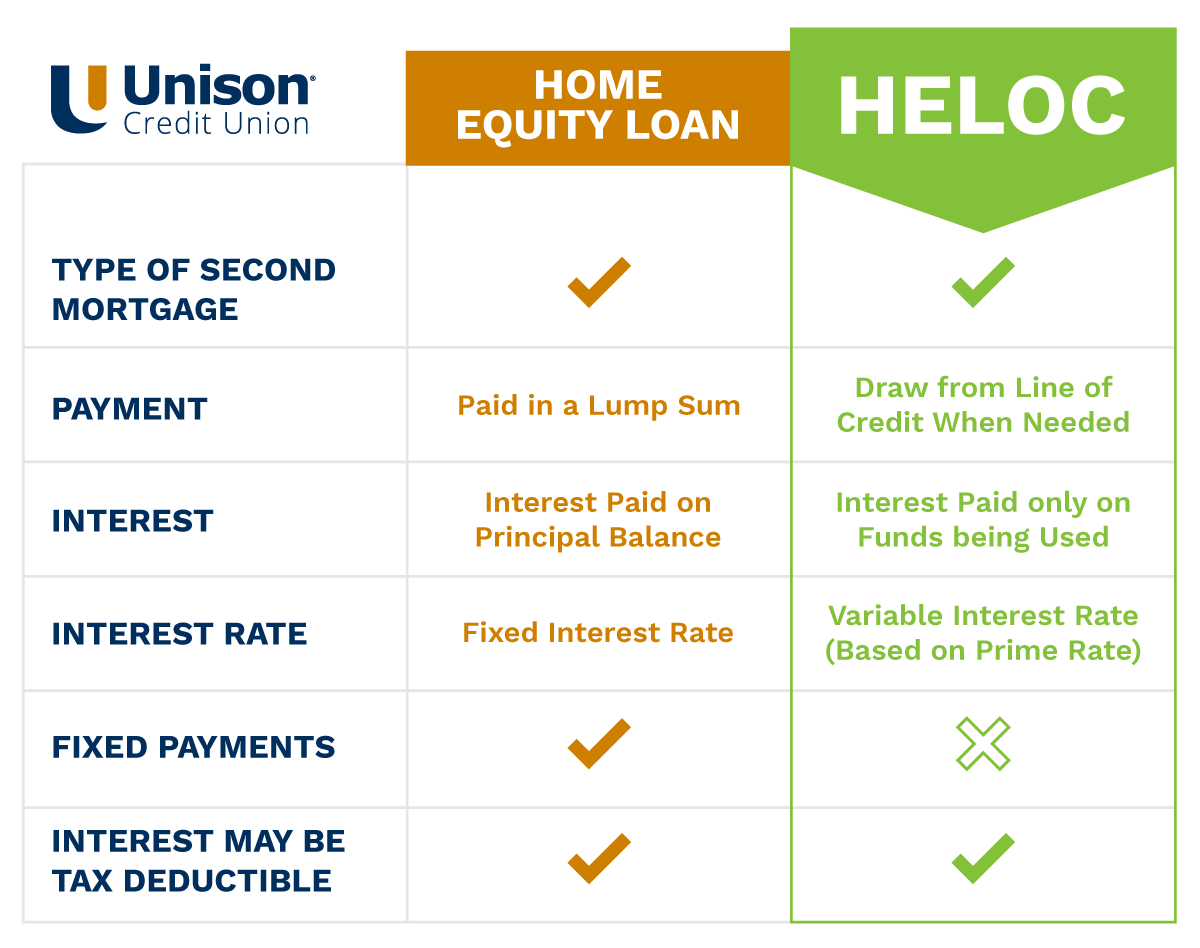

HELOCs vs. Home Equity Loans

Both a HELOC and a home equity loan let you access the equity you’ve built through the purchase of a home, which is something you typically only get when you sell your house.

Both a HELOC and a home equity loan let you access the equity you’ve built through the purchase of a home, which is something you typically only get when you sell your house.

A home equity loan is delivered as a lump sum, which gets paid back over a fixed term, similar to your primary mortgage.

“A HELOC is often compared to a type of second mortgage. Although, people who’ve paid off their home can also use it as a financial option,” says Arnoldussen. “But, instead of being a fixed loan amount, it uses your equity to provide you with a line of credit that you can draw funds from as you need them.”2

Home equity loans have fixed interest rates while rates for HELOCs are typically adjustable as they are based on the prime rate each month.

Erika Arnoldussen, Unison Credit Union Branch Manager

“A major advantage of a HELOC is that you only pay interest on the funds you’re using,” Arnoldussen explains.

For example, if you took out a $50,000 home equity loan, you’d pay interest on the balance of the loan until it’s paid off. If you had a $50,000 HELOC, and you used $10,000 of it, you would only pay interest on the amount withdrawn.

“That’s why I often advise Unison members not to transfer the full amount of the credit line into their account right away,” adds Arnoldussen. “Why pay interest on it when the funds can just sit there until you need them?”

Furthermore, when you pay off that $10,000 from your HELOC, the full $50,000 line of credit becomes available to you again. It’s much more flexible than a home equity loan.

Another way in which HELOCs and home equity loans are similar is that you must pay off the balance when you sell your home. Also, falling behind on payments on either could lead to foreclosure. That’s why we always advise members to use HELOCs responsibly.

Four Beneficial Ways to Use a HELOC

Arnoldussen says a HELOC can be used for just about anything. Although, there are a few popular ways that credit union members get the most value out of HELOCs.

1. Home Improvement Projects and Updates

According to Arnoldussen, completing projects in their homes is the top reason Unison members apply for a HELOC.

According to Arnoldussen, completing projects in their homes is the top reason Unison members apply for a HELOC.

“By having that line of credit available to them, they’re able to finally get those home improvement plans that have been on their list done, which can be a relief,” she says.

The convenience of withdrawing only what’s needed is perfect for major updates to your home, especially when you may not be completely sure how much you’ll need to get the job done.

Whether it’s a kitchen remodel, an updated bathroom, financing a home gym, or your very own Green Bay Packers themed rec room, you can keep accessing that line of credit and paying down the balance so you can move on to the next project.3

As of this writing, if you are using a HELOC to make improvements to your home or property, the interest you pay is tax deductible.4 HELOC deductions are limited to interest paid on debt of no more than $100,000 or the purchase price of the home if that was less than $100,000.

2. Paying for College

Another popular reason to apply for a HELOC is to cover the costs of college education. In fact, a HELOC may have a lower interest rate than some student loans, making it an attractive option for financing higher education.

Another popular reason to apply for a HELOC is to cover the costs of college education. In fact, a HELOC may have a lower interest rate than some student loans, making it an attractive option for financing higher education.

“I work with a father who has three kids in college at the same time,” Arnoldussen says. “Every semester he has to send checks out to help them pay tuition. He can afford to pay it himself through bonuses he gets from his job, but those bonuses don’t always line up with tuition bills. So, he uses his HELOC until the bonus comes in, and then he can pay off the balance.”

3. Paying off High Interest Debt

While Arnoldussen says it is less common, some of our credit union members use HELOCs as an effective way to pay off debt with high interest rates.

While Arnoldussen says it is less common, some of our credit union members use HELOCs as an effective way to pay off debt with high interest rates.

The average APR for credit cards is around 16%, which is significantly higher than rates you’ll get with a HELOC. The lower interest rates help people who consolidate their debt pay it down faster.

What you don’t want to do is immediately start running up credit card debt after paying it off using a HELOC. Unison Member Advisors can work with you to develop a stable and responsible plan that leads to financial freedom.

4. Financial Safety Net

“Sometimes people will get a HELOC after their mortgage is paid off so they have a backup plan or a financial cushion, just in case unexpected expenses, such as the need for a new roof, come up,” says Arnoldussen.

“Sometimes people will get a HELOC after their mortgage is paid off so they have a backup plan or a financial cushion, just in case unexpected expenses, such as the need for a new roof, come up,” says Arnoldussen.

Having an emergency savings is important, yet many people struggle to set enough money aside. HELOCs can be a reliable way to make sure you have money in case of an emergency, which could include costly vehicle repairs, medical expenses, the loss of a loved one, or replacing your home’s furnace in the middle of a harsh Wisconsin winter.

“Occasionally, we notice Unison members who come in often for smaller personal loans,” says Arnoldussen. “We let them know a HELOC is available. This way they don’t have to come in and repeatedly go through the process of applying and signing for loans because that line of credit is there when they need it for unexpected expenses.”

Lock Down a HELOC with Unison Credit Union

Arnoldussen finds one of the most common questions she gets from those applying for a HELOC concerns the payment amount.

“At Unison, the minimum payment is just 1% of the outstanding balance,”5 she says. “But, you can pay off as much as you want because there are no pre-payment penalties. Plus, we offer bi-weekly payment options. You also do not need to have your primary mortgage with Unison to apply for a HELOC through our credit union.”

The total amount of the line of credit can go up to 80% of your home’s value, and you will need to get your house appraised during the application process, which typically cost a few hundred dollars. Unison requires members take out a minimum $5,000 line of credit with a HELOC. The first draw must be a minimum of $1,000, but after that it can be whatever amount the member needs up to the credit limit.

In addition to the home appraisal, we will also need to pull your credit. Arnoldussen says Unison Members will need to see the following documentation and information when you apply for a HELOC.

- Mortgage statement showing balance of first mortgage, if applicable

- Most recent property tax bill

- Proof of homeowner’s insurance

- Income and employment information

- Deed or legal description of property

Arnoldussen says the most convenient way to access your HELOC is to use online banking to transfer money directly into your checking or savings account as you need to spend it.

Stop in at one of our six convenient locations to speak with a Unison Member Advisor and learn more about how a HELOC could work for you. Check out our most recent rates or give us a call at 888-878-8806 today. Let Unison Credit Union empower you with financial flexibility!

1Minimum 20% remaining home equity required. Subject to credit approval. 2During the 72 month draw period. 3During the 72 month draw period, after which the balance must be repaid. 4Everyone’s situation is unique. Consult a tax professional for advice. 5Minimum payment is the great of $50 or 1% of the outstanding balance at the last advance during the draw period. After the 72 month draw period, the minimum payment during the repayment period if the greater of $50 or 1% of the outstanding balance at last draw plus unpaid finance charges that have accrued on the remaining balance. A periodic interest finance charge is imposed on all Loan Advances; HELOCS are a variable Mortgage Loan product – the annual percentage rate may vary after the account is opened. Closing costs depend on the age of the last appraisal and amount borrowed; typical closing costs range between $151 and $700. Other fees and conditions apply; see a Member Advisor for details. Non-promotional Index is the highest Prime Rate published in the Wall Street Journal on the first day of each calendar month; currently 5.000%, with a floor of 4.000%, an annual increase cap of 2.000% and a lifetime maximum cap of 18%. HOME MORTGAGE DISCLOSURE ACT NOTICE The HMDA data about our residential mortgage lending are available for review. The data show geographic distribution of loans and applications; ethnicity, race, sex, and income of applicants and borrowers; and information about loan approvals and denials. Inquire at this office regarding the locations where HMDA data may be inspected. Unison Credit Union 920.766.6000.Unison Credit Union does not knowingly collect, maintain, or use personal information from our website about children under age 13. If a child whom we know to be under age 13 sends personal information to us online, we will only use that information to respond directly to that child, notify parents, or seek parental consent. FEDERALLY INSURED BY NCUA.

Unison Credit Union does not knowingly collect, maintain,

or use personal information from our website about children

under age 13. If a child whom we know to be under age 13

sends personal information to us online, we will only

use that information to respond directly to that child,

notify parents, or seek parental consent.

FEDERALLY INSURED BY NCUA.

Unison Credit Union does not knowingly collect, maintain,

or use personal information from our website about children

under age 13. If a child whom we know to be under age 13

sends personal information to us online, we will only

use that information to respond directly to that child,

notify parents, or seek parental consent.

FEDERALLY INSURED BY NCUA.